February and Marchmarked an unexpectedly optimistic period for U.S. manufacturers,during which confidence improved steadily amid burgeoninggeopoliticalvolatilityanda developingsupplycrisis overseas. This month, however,thestressors ofinternationalconflict and rising priceshave finallycastashadowover confidence in the business environmentin the sector.

According toChief Executive’s latest CEO Confidence Index Survey, fieldedApril7-9among 416U.S. CEOs, U.S. manufacturersare showing moderation: Theyrate current business conditions a5.5 out of 10, on a scale where 1 is Poor and 10 is Excellent––on par with February2026figures.While down 4 percent since March, thisratingisstill higher than where the Index began the year (5.3out of 10).

When asked how that may changeover the next 12 months, manufacturers say they expect improvedconditions,projecting business conditions will rise to 6.0 out of 10 by this time next year.Down 3 percent sinceMarch,this forecast hovers around where itsatthe first two months of the year.

Non-manufacturers followed a different trend yet againin April, withcurrent ratingsholding steadyat 5.5out of 10 and future forecastsincreasing 3 percent since March despitebeing presented withthe sameset ofstressors as theirmore pessimisticpeers.

When asked to explain the core driving factors behind their forecasts, U.S. manufacturerslargely hadtwo things to say:the supply chain effects of instability abroad andconsumer behavior.

Some specifically noted the rising costs of fuel as integral to their economic outlook:“Geopolitics and the increased cost of energy is and will continue to have a negativeimpact on virtually all aspects of the economy,” says John W. Gessert,CEO ofAmerican Plastic Toys, a mid-sized consumer manufacturing firm headquartered in Michigan.

Chris Highfield, President ofPennant Moldings, a family-owned industrial manufacturing firm,agrees,alsohighlightingthe pressure of decreasedconsumer spending:He notes “uncertainty with the Iranian conflict” and “rising costs driven by fuel pricing and [a] reduction of disposableincome as consumers spend less” as integral to his projection.

Other manufacturers describe a struggle to accurately conduct long-term planningunder such turbulent conditions. Peter Ensch, CEO ofSani-Matic, a large-sized manufacturing firm with international operations, says “there continues to be too much uncertaintylargely driven by the current administration’s changes in direction, tariff/trade policy and geopolitics that make it very difficult to develop andimplement longer term planning.”

All in all, manufacturers are less dividedin their driving factors than they were last month, when they could beroughlysortedby their focus on long-term versus short-term goals. This month,nearly three-quartersof manufacturing CEOsnoted geopolitics in some regard,tying the sector together and defining itself clearly as a core issue.

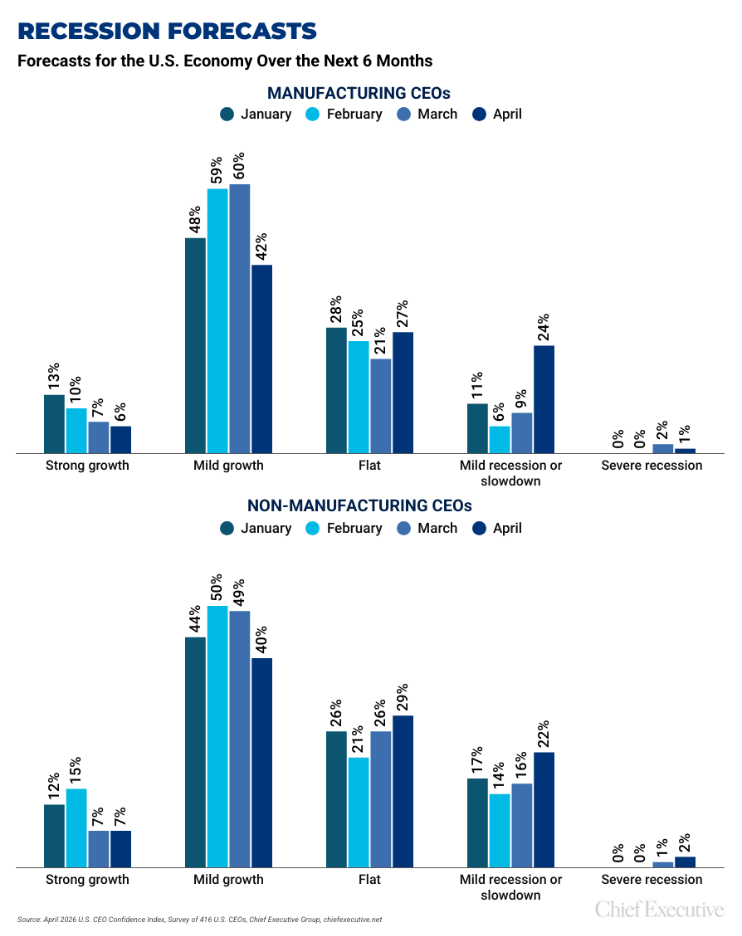

Recession forecasts show a significantly negative turn for manufacturers this month:25 percentexpect some kind of recession in the next six months,a staggering127 percentincreasesince March(when just11 percent expected the same). The proportion of manufacturers projecting growth decreased in tandem, from67 percentin March tojust48percentin April.Nonetheless, the largest proportion still shares a positive outlook,indicatingmoderationin response to stressorsinstead ofa nosedive.

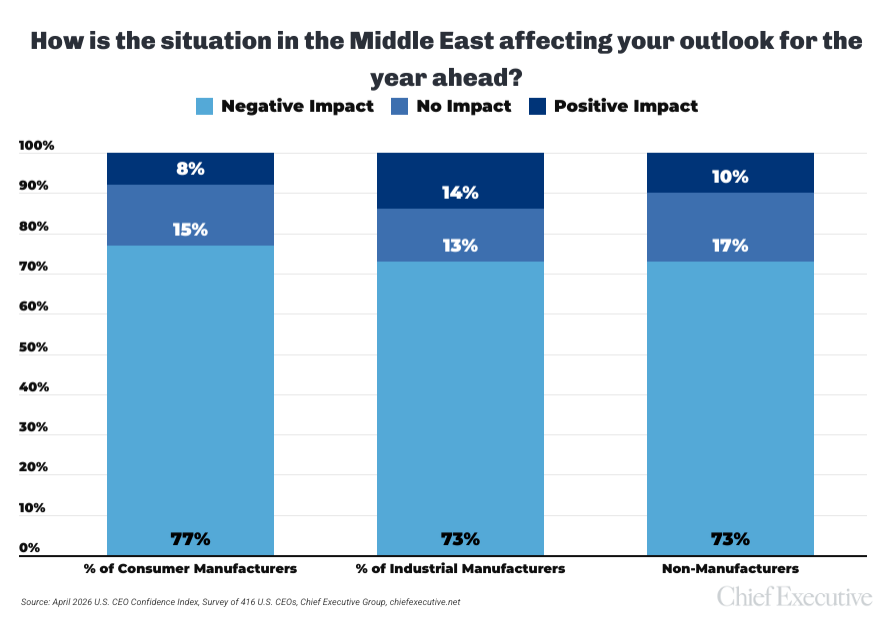

When it comes to the situation in the Middle East, there is asubtledivide in the sector: 77 percent of consumer manufacturers report negative impacts, in comparison tojust73percent of their industrial-focused peers.While geopolitical volatility centered in this region is clearly acorefactor for both groups, thelonger cycles and B2B structure of many industrial manufacturers isperhaps providingthemsome insulation from the turbulence.

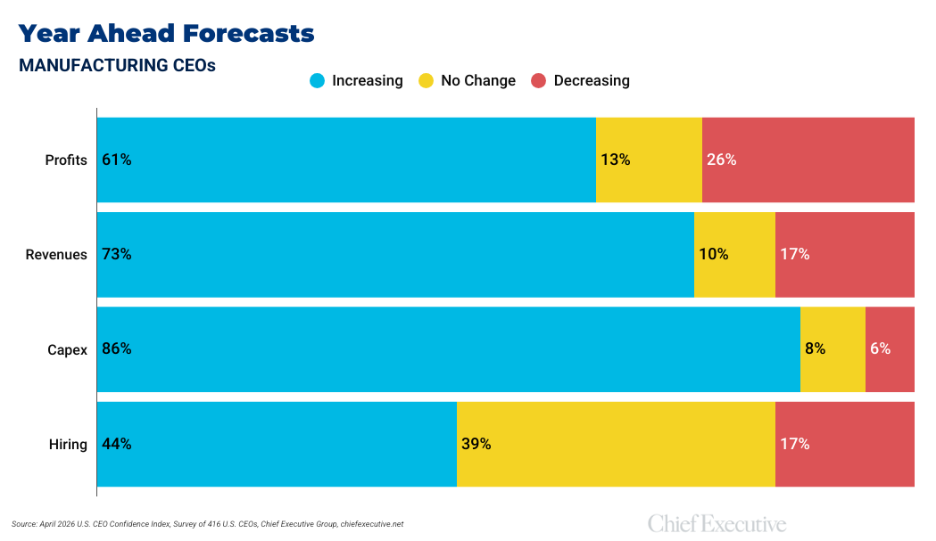

Though business confidence forecasts followed a pattern of moderation, year-ahead forecasts saw some of the largest decreasesin months:

- 61 percent of manufacturers forecastprofitsto increasein 2026 vs. 2025 (down from 74 percent last month)

- 73 percentexpectrevenuesto increase this year (down 10 percent since March)

- 44 percent plan to add to theirheadcountin 2026 (down from 57 percent last month)

Thepercentage of those planning to add to theircapital expenditurestook afascinatingturn this month,increasingby 65 percentas the other categoriesfell:86 percent now plan increases, in comparison to just52 percent in March.This is potentially a signal of structural changefor some, as manufacturing firms invest in internal development to navigate the year ahead.

About the CEO Confidence Index

Since 2002, Chief Executive Group has been polling hundreds of U.S. CEOs at organizations of all types and sizes, to compile our CEO Confidence Index data. The Index tracks confidence in current and future business environments, based on CEOs’ observations of various economic and business components. For additional information about the Index and prior months data, visit ChiefExecutive.net/category/CEO-Confidence-Index/