The combination of international conflict, price volatility, regulatory change and looming inflationary conditions hascreated a multi-pronged threat for manufacturing leaders sincelate 2025. While those stressors continue to cast a dark shadow overtheircurrent businesssentiment,mostU.S. manufacturersare convinced that resolve is to come in the year ahead.

According toChief Executive’slatest CEO Confidence Index Survey, fielded May 5-6 among 342 U.S. CEOs,manufacturers are holding steady, rating current business conditions a 5.5 out of 10, on a scale where 1 is Poor and 10 is Excellent. The Index has hovered around this 5.5/10 rating since February 2026,when the conflict in the Middle East intensified and supply chain effects became a core concern for manufacturing leaders.Nonetheless, the Indexis stillin a better placethan it was throughout most of last year.

When asked how that may change over the next 12 months, manufacturers say they expect improvedconditions,forecastingtheywill rise to 6.0 out of 10 by this time next year.Up 2percent since April, thisturntoward optimism—an outlook that 52 percent of U.S. manufacturers share—has recovered some of the losses feltwhen the Index fell 3 percent last month.

Manufacturers continue to follow a different patternthan the majorityof CEOs polledin May, withoverallratings of current conditions improving slightly andfuture forecastsdeclining 1 percentsince April as more CEOs adopt a “wait and see” perspective.

Some manufacturers attribute their shift toward optimism to improved demand, especiallyin thetechnologyand consumer productssub-sectors, and the presence of indicators that volatility will resolve before 2027.

Randy Colwell, CEO of the mid-sized industrial manufacturer Holloway America, sharesa perspective polarized by thecontinuityof current stressors, yet nonetheless hopeful for resolve: “Right now, our market … is strong [and] material costs are steady, but higher interest rates and fuel costs may worsen the market. … Especially if thewar in Iran slows, we see good growth in the next 12 months.”

Others agree: “I believe the interest rates will be lower [in the year ahead] … also, the tariff refund will drive growth,” says Art Hamilton,president of the mid-sized industrial fabrics manufacturer Hamilton International.

Still, other manufacturers hope for a “slowdown in accelerating costs” and “growing market share through innovation.”

That optimistic conviction has produced an improvement in recession forecasts in May, after they dramatically worsened last month with atriple-digit increase in the proportion of manufacturers expecting a recession.Exactlyhalfproject growththis month, up from 48 percent last month. While the proportion still forecasting recessionary conditions is sizeable at 23 percent,thisisnonetheless animprovement from April’s 25 percent.

Although non-manufacturers took a more pessimistic turn when it comes to Index forecasting, they continue to be more optimistic than their peers. 53 percent now expect some kind of growth in the next six months, up from 47 percent in April.

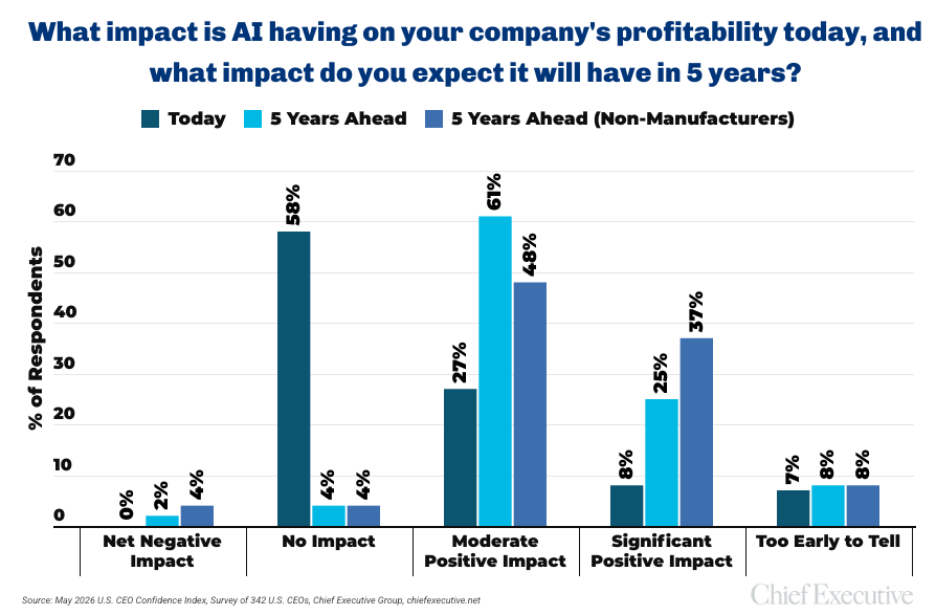

One of the necessarytools manufacturing leaders are using to navigate this turbulent environment is undoubtedly artificial intelligence, and they are bullishon its capabilities for improving profits by 2031.

When asked about the level of impact AI has on current company profitability,mostU.S. manufacturers (58 percent) reported that it hasno impact. Thisreflects,perhaps,thefact that many organizations are stillin theprocess of onboardingAI technologies and clearly defining how they can produce a ROI.

When the time span changed, however,mostmanufacturing CEOs shareda different perspective:86percent forecast that AI will have some kind of positive impact on profitability5 years from now, with the majority describing that impact as moderate.

Non-manufacturers, in comparison, tend to beevenmore bullish on AI: 37 percent forecast a significant positive AI-drivenimpact on profitability5 years down the line.

A slim minority of either group forecast net negative effects related to AI by 2031: 2 percent of manufacturers and 4 percent of non-manufacturers.

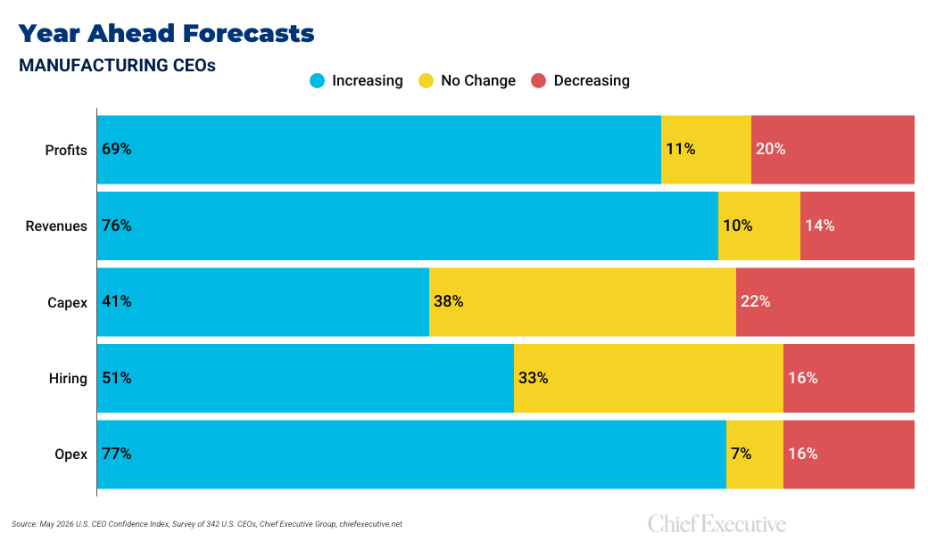

Year-ahead forecasts are healthily optimistic this month, after several categories suffered losses in April:

- 69 percent of manufacturers forecastprofitswill increase in 2026 vs. 2025 (up from 61 percent last month)

- 76 percent forecastrevenuesto increase this year (up from 73 percent in April)

- 41 percent plan to add to theircapital expenditures(down from 86 percent last month, when manufacturers were unusually optimistic)

- 51 percent plan to add to theirheadcountin 2026 (up from 44 percent in April)

- 77 percent foresee additions to theiroperating expenditures(a new category returned to in May)

About the CEO Confidence Index

Since 2002, Chief Executive Group has been polling hundreds of U.S. CEOs at organizations of all types and sizes, to compile our CEO Confidence Index data. The Index tracks confidence in current and future business environments, based on CEOs’ observations of various economic and business components. For additional information about the Index and prior months data, visit ChiefExecutive.net/category/CEO-Confidence-Index/